August Apartment Market Update

For apartment owners and operators: Summer 2025 is likely to go down as the worst summer for apartment rents since the Great Financial Crisis. And that isn’t hyperbole… though it does warrant some asterisks marks and some context…

Here’s the key stat:

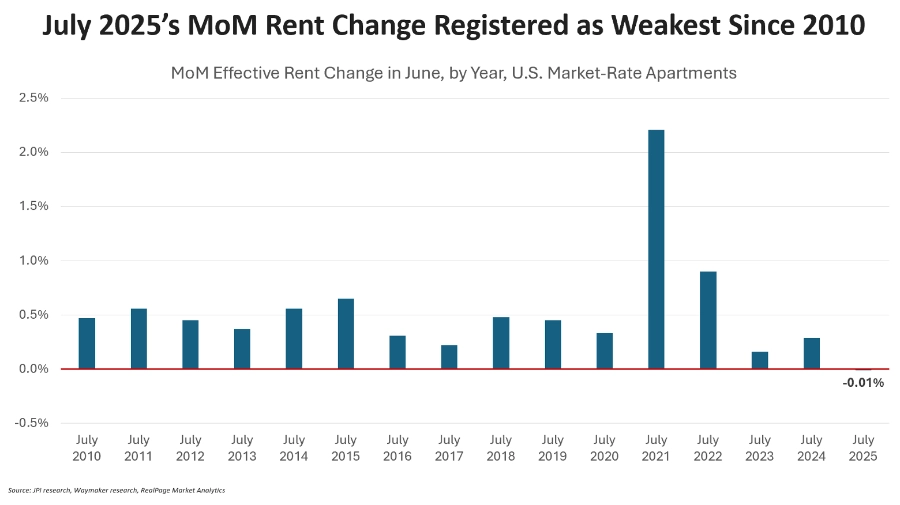

- Apartment rents in July fell (very, very slightly) 0.01% month-over-month. That’s the weakest July number since prior to 2010, according to RealPage Market Analytics data.

- That followed June’s 0.19% increase, which was the second-lowest bump for any June since 2010. The only year worse: June 2020 (remember that year?).

- The followed May’s 0.33% increase, was also the second-lowest bump for any May since 2010 … with only May 2020 being softer.

So barring a tidal wave in August (highly unlikely), that’s how you could conclude summer 2025 will be the U.S. apartment sector’s weakest summer since the GFC.

BUT … I did say the statement deserved some asterisks marks and context, right? What makes summer 2025 not really comparable to the GFC is that most key apartment indicators (other than new lease rents, of course) are strongly positive. Consider:

- The rent slowdown is ONLY on the new lease side. Renewal rents keep steadily growing at a normalized rate of 3.8% as of July.

- Solid renewal rent increases are NOT prompting move-outs. It’s the opposite, actually. Retention remains elevated at 56.2%, up 50 bps year-over-year and up about 200 bps compared to the 10-year average.

- Apartment demand remains robust … BUT most of that net new absorption is going to newly built units in lease-up. That means it’s still a very competitive environment to compete for leasing traffic.

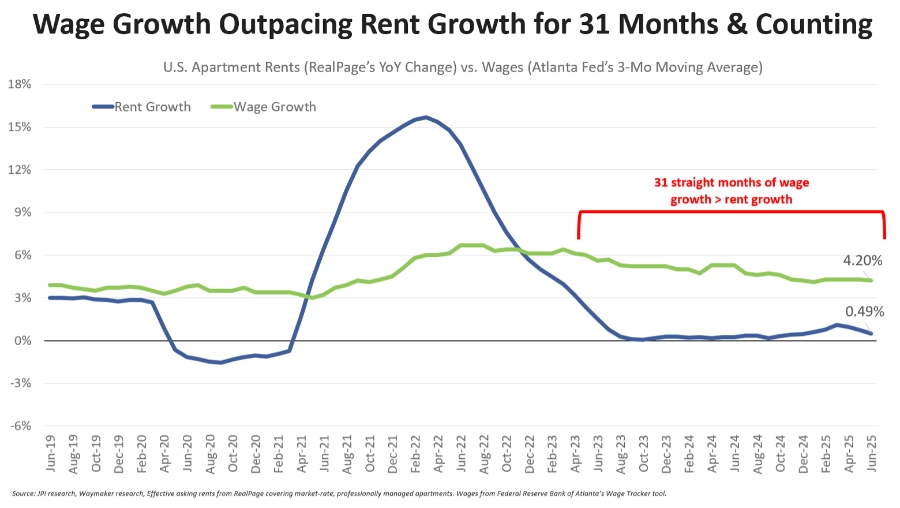

- Apartment affordability continues to improve, with wage growth outpacing rent growth of 31 straight months. Rent-to-income ratios among households signing a new market-rate apartment lease fell to 21.6% in July. That’s back in the pre-pandemic range. The REITs are reporting favorable affordability trends, too.

- Therefore: Vacancy held steady in July (according to both CoStar and RealPage)

What’s happening? Some thoughts:

It’s a Hyper Competitive Leasing Environment … and Macroeconomic Uncertainty Doesn’t Help

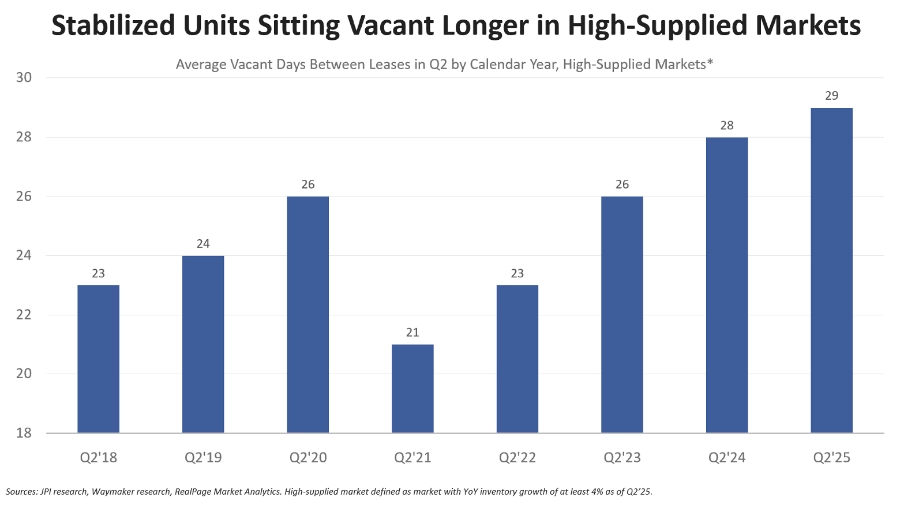

I won’t repeat everything I wrote last month, but the same themes are still likely true: There’s a ton of supply in active lease-up, much of which is offering generous concessions. In turn, concessions (and true rent cuts) are coming among many stabilized properties too — as they compete to hang on to renters and protect occupancy. We continue to see vacant units sit on the market longer than usual, specifically in higher-supplied markets.

Of course: Weak consumer confidence likely plays a role. Not only among prospective renters potentially nervous about the economy. But also among apartment operators strategically choosing to protect occupancy (and cashflow) over pushing rents.

This, too, was a theme on REITs’ earnings calls this past quarter. NexPoint’s Matt McGraner said this on their call: “In late June and July, we have seen new lease growth slow modestly as operators remain defensive amid economic uncertainty and soft consumer sentiment.”

For more details on the current state of the multifamily market and the outlook, here are some other resources:

- The Rent Roll podcast: 5 Takeaways from the Apartment REITs’ Earnings Calls, with special guest Rich Hightower of Barclays.

- Also The Rent Roll podcast: Q3 Apartment Market Update & Outlook with special guest Matt Vance of CBRE.

- Rental Housing Economics newsletter from July and June.

More Highlights on Apartment Trends:

- CoStar’s new head of multifamily analytics, Grant Montgomery, wrote that demand should exceed supply by year-end 2025.

- RealPage reported that new lease rent growth topped 3% in only six major U.S. metro area as of July: San Francisco, Chicago, Pittsburgh, New York, Cincinnati and San Jose. On the flip side, rent cuts exceeded 4% in Austin, Denver, Phoenix and San Antonio.

- Apartment List, too, ranked San Francisco as the top rent growth market — while also noting Fresno and Chicago in the top 3. Yardi had Chicago, Columbus and Detroit as their top 3.

- Looking at the city level, CoStar reported top rent growth in Brookline, MA; Chicago, IL; Brooklyn, NY (well, a borough not a city but we’ll give them a pass); Seattle, WA; and Columbus, OH.

- Yardi Matrix reported positive news on apartment operating expenses: “Expense-related pains eased, as costs climbed just 1.3% and 1.7% per market-rate and affordable unit during the first half of 2025.”

- Apartment List reported an interesting stat among their users: “Low urgency is the dominant search mindset this summer leasing season. More than half (54%) of Apartment List users are browsing without a firm move-in date, an all-time high. It’s a sign of confidence and caution coexisting: renters know they have options, and they’re using that to their advantage.”