April Multifamily Market Update: Spring Leasing Season Is Off to a ‘Ho-Hum’ Start

Going into the spring leasing season last month, I wrote this: “Spring is always critical in the apartment business, of course. But it kinda feels even MORE important here in 2026.”

So now that we’re in the heart of the spring leasing season, how does it look so far?

Well, the word “ho-hum” comes to mind.

It’s not bad by any means. If you were worried the tepid job market would freeze up apartment demand, that hasn’t happened. But if you hoped to see a big spring rebound, that didn’t happen, either. It’s … okay.

Apartment demand has been very solid. Just not enough to put a big dent in vacancy rates elevated by the massive 2023-25 supply wave.

Rents did increase in March. Just not as much as we typically see this time of year.

As my friend Grant Montgomery at CoStar wrote: “The modest gains in March point to a more gradual early-season recovery than is typically observed, as supply conditions remain a constraint on rent growth nationally.” That’s the story.

Let’s break down the numbers.

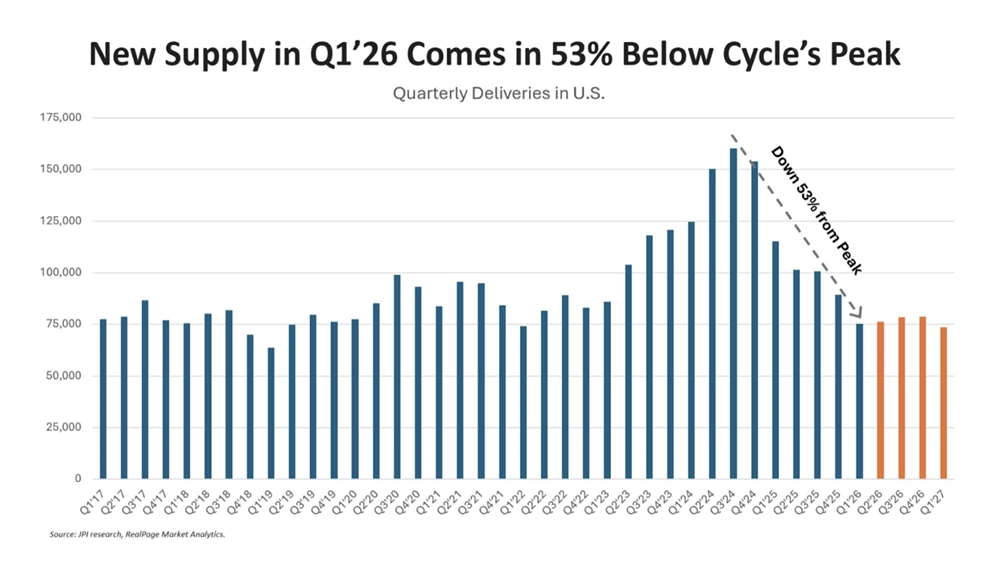

Supply: The Drop-Off Is Here

As expected, supply plunged in Q1 2026. (Finally, right?) Q1 2026 came in as one of the lowest supplied quarters since 2018, with 75,000 units completing, down 53% from the peak set back in Q3 2024. That’s the first time in four years that quarterly deliveries came in below 80,000 units. So, supply isn’t totally evaporating, but it’s dropped off significantly. And we should see similar numbers through 2026.

That drop is basically universal, extending not just to the Sun Belt but even to lower-supplied markets in the Midwest.

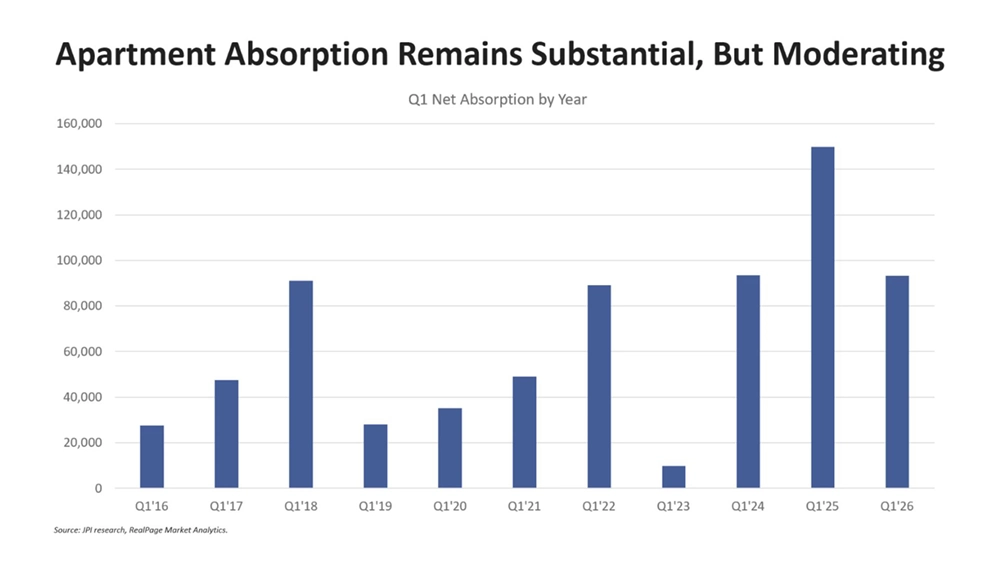

Demand: Still Cooking, Even If at a Lower Temperature

If you looked at Q1 in a vacuum, you’d say the absorption number—around 90,000, according to RealPage—is good. The broader story is pretty similar, too, in that there are good, solid numbers that, in a vacuum, make for a solid Q1. But obviously, we aren’t operating in a vacuum. And solid numbers look unspectacular when you have a big hole to dig out of—that hole being the supply overhang from 2023-25 that drove up vacancy rates.

So, most apartment operators probably wanted a stronger start to 2026, enough to put a bigger dent in vacancy and regain some pricing power. That didn’t really materialize.

But at the same time, we should also point this out: Apartment absorption generally depends on job growth (even if the correlations are very messy). And even absent much job growth in most markets—and all the worries about the impacts of AI, the Iran conflict, low consumer confidence, etc.—we still saw very solid absorption in Q1.

And where’s that demand going? Well, the usual suspects dominate the leaderboard: Dallas, Phoenix, Atlanta, Charlotte, Austin, and Orlando. (Houston has been a notable exception as of late.) But outside the Sun Belt, we also have big numbers in New York, Northern New Jersey, Columbus, and Philadelphia.

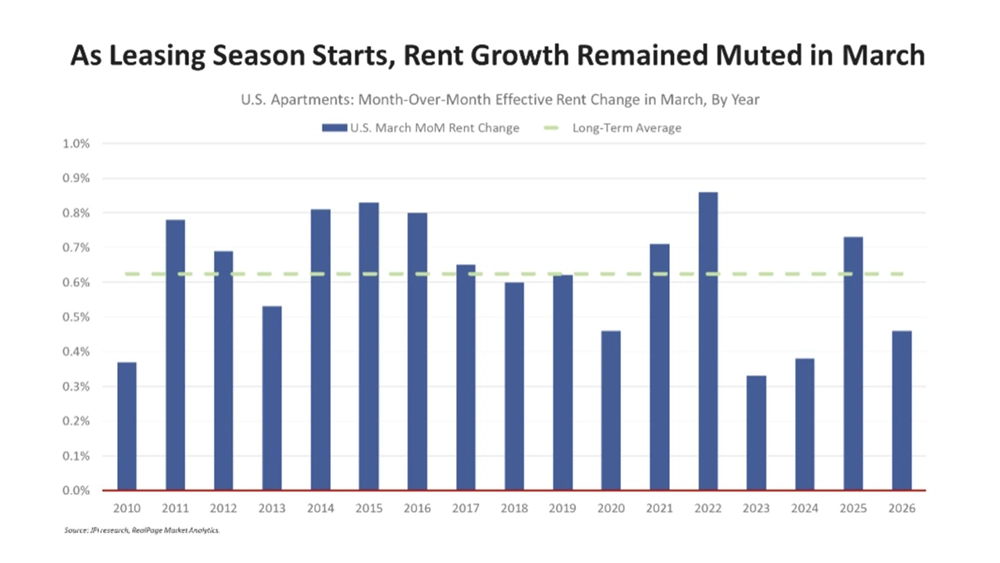

Concessions and Rent: It’s Still a Renter’s Market

With improving affordability (wage growth topping rent growth for 38+ straight months) and ample options (on the heels of the largest supply wave in nearly a half-century), apartment renters retain the upper hand.

That means operators remain in an ever-extending occupancy build-up mode, pushing rents more modestly than usual for March. Concessions remain abundant, with no sign of a pullback yet.

Rents did, indeed, increase in March, but not much—just 0.46% compared to February. But that’s almost 20 bps below the long-term norm for March. Year-over-year rent change remained even weaker at -0.7%, according to RealPage (or +0.4%, according to CoStar).

Regional Storylines

Regionally, the storylines haven’t changed much. Rent trends are improving across most of the country, but at a very gradual pace.

San Francisco remains atop the leaderboard, with rents up 9% year-over-year, followed by next-door San Jose at 5%. On the other side of the country, one market that has snuck up the leaderboard is Virginia Beach, now topping 4%. New York, Chicago, Milwaukee, and Cleveland also ranked high.

On the flip side, the usual suspects still pull up the rear: Austin, Denver, San Antonio, and Phoenix. And then they’re joined by Tampa, which has lost considerable momentum over the past year. Rents in Tampa dropped 5.6% year over year. That’s a massive change from just one year ago, when Tampa ranked among the few major Sun Belt markets with positive rent growth. That traces to weakening demand and occupancy losses, particularly in the second half of last year.

Another market to keep an eye on is Houston. This one puzzles me, and candidly, I expected to see better numbers by now. There’s not a ton of supply there relative to other Sun Belt markets—plus, the latest Census data shows Houston was the fastest-growing metro area by population growth in 2025. Yet, apartment absorption really dropped way down over the same time period. So, that means population growth isn’t translating to household formation—at least not yet—and maybe more immigration impacts in certain parts of the market. (I still think Houston could turn the corner, given strong demand drivers plus moderate supply. Just not sure when that happens.)

Here’s the bottom line: We’re in the heart of the spring leasing season now, and the balance of power is still very much with the renters. They’ve got more options thanks to all this supply, and that means it’s still a competitive leasing environment in most of the country.

If you thought we’d see the balance of power shift by now due to falling supply, remember this: Deliveries are down in 2026, yes, but that massive supply wave from 2023-25 still has to lease up and stabilize before we can see vacancy rates normalize. And that likely has to happen before we see operators regain pricing power.