May Multifamily Market Update: Is the Apartment Market Heating Back Up?

No one is popping champagne just yet—we’re still a long way from that—but the tone around apartment leasing is starting to improve. We heard it on the recent round of REITs’ earnings calls, and we saw some signs of it in recent market data, as well.

It’s a gradual step up from my summation last month that spring leasing was off to a “ho-hum start.” Not bad, not great. Here in May, it feels like we’re somewhere between “ho-hum” and “humming along.”

Here are some of the positive indicators.

First, REITs took a more bullish tone in their recent earnings calls, with most reporting stronger numbers for April while teasing better numbers to come later this year. That’s true even in the higher-supplied Sun Belt region. Camden CEO Alex Jessett said its occupancy rates were up 30 bps in April and its blended rent growth accelerated by 100 bps. IRT’s James Sebra said, “April and May renewal trade-outs are tracking modestly ahead of plan.”

Some of that is seasonality, of course. The spring leasing season is supposed to be better than Q1. But it’s encouraging to see that momentum actually happening, even as the job market remains choppy and consumer confidence low. The long-awaited supply drop-off is translating to improved momentum so far.

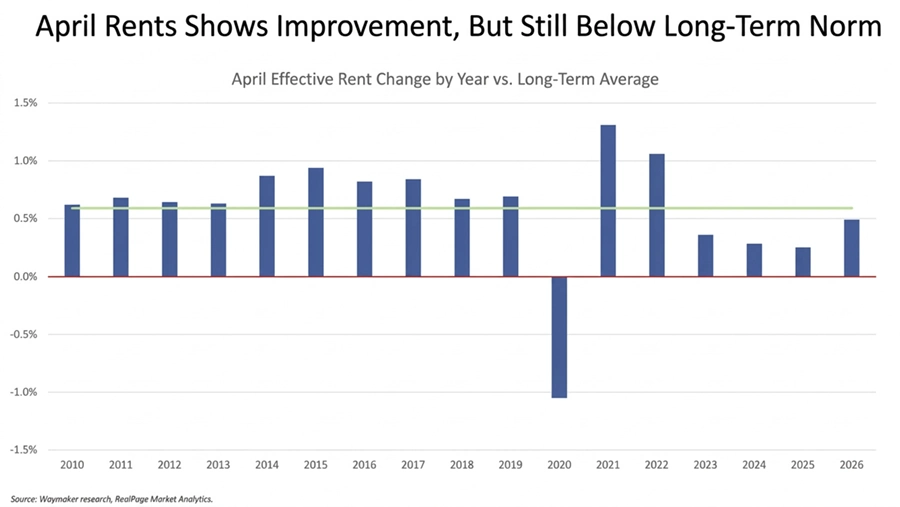

Indeed, April month-over-month rent growth came in at 0.5%, according to RealPage, which was a four-year high for April, though still below the pre-pandemic norm of 0.7%. Most markets, from the Sun Belt to the coasts and the Midwest, saw the same pattern. Additionally, occupancy rates improved 40 bps nationally through March and April combined, thanks to falling supply. While absorption is moderating, too, supply is dropping off faster, allowing occupancy rates to tick upward.

To be fair, you may recall that we heard similar stories one year ago. Then, the tone suddenly deteriorated around May and into the summer and fall.

If you think back to spring 2025, we heard a similar story back then. Is 2026 different? We’ll see, but I think there are a couple key differences. First, we still had a lot of supply delivering last year. It was the third-highest supplied year since the mid-1980s (behind only 2025 and 2024). And secondly: The spring 2025 bounce really came from one remarkably strong month (March) that wasn’t sustained. Here in 2026, we’ve now seen more than two months of steadier improvement.

MAA’s Tim Argo added some good color on the spring 2025 versus spring 2026 comparison on MAA’s recent earnings call: “I would say we’re seeing a more seasonal or more normal acceleration in new lease rates this year. Last year, it was a little quicker, but then it slowed to a complete halt. … We look at where we are with exposure, where we are with lead volume, where we are with occupancy, and seeing what’s out there with pre-leasing, we would expect that momentum to continue beyond May, unlike it did last year.”

Let me close this section with this: The apartment market is trending in the right direction, but it remains a bumpy path and an uneven recovery depending on location, property type, management execution, etc. As Yardi stated in their most recent report: “While this improvement is not yet broad-based or sustained, it suggests conditions may be beginning to turn a corner, though a gradual recovery is still expected.”

But considering ultra-low consumer confidence, challenges for recent college graduates finding jobs, and broader economic uncertainty, you could make the case that U.S. apartments are holding up decently well—and perhaps better than some anticipated.

What’s Ahead?

If you listened to the REITs’ recent earnings calls, you’d sense increased optimism for the outlook. Maybe “cautious optimism” is the best term given lingering broader uncertainty. But check out these comments from REIT execs stating a clear readiness to start pushing on rents.

Essex’s Angela Kleiman: “Heading into peak leasing season, we have shifted our operating strategy to driving rent growth across most markets, and our portfolio is well positioned with April financial occupancy at 96.4%.”

IRT’s Scott Schaeffer: “Our recent strategy of prioritizing occupancy now positions us to prioritize rental rate growth during the upcoming leasing season.”

Camden’s Alex Jessett: Because of improved pricing power in areas with reduced supply, “that makes us feel very good about our ability to get positive rent growth as we move through the year.”

UDR, AvalonBay, MAA, and Equity Residential all made similar comments. Will that acceleration materialize? We’ll see. But the tone is clearly more bullish than previously.

Market Highlights

The usual suspects continue to lead the nation in rent cuts: Austin, Denver, San Antonio, Phoenix. But Tampa recently joined that group, too, losing considerable momentum since the second half of 2025 due to demand-side softness. Rent growth in Tampa was mildly positive at one point last year, but is now -5.3% year-over-year, according to RealPage.

The Bay Area boom continues thanks to low supply, AI jobs, and improved quality of life issues. San Francisco rent growth surged up to +9.6%, while San Jose ranked second nationally at +5.0%. And now that boom is spilling over to the East Bay (finally), after a long lull. The Oakland area now ranks seventh with rent growth of 2.9%.

Other hot spots for rent growth: Virginia Beach, New York, Milwaukee, Chicago, and Minneapolis.