June Apartment Market Update: Why is Rent Growth Backtracking Again?

Through the first quarter of this year, it looked like mainstream thesis was playing out perfectly for the apartment industry: Strong demand and modestly upward rent momentum suggesting a bigger rent rebound as supply levels drop.

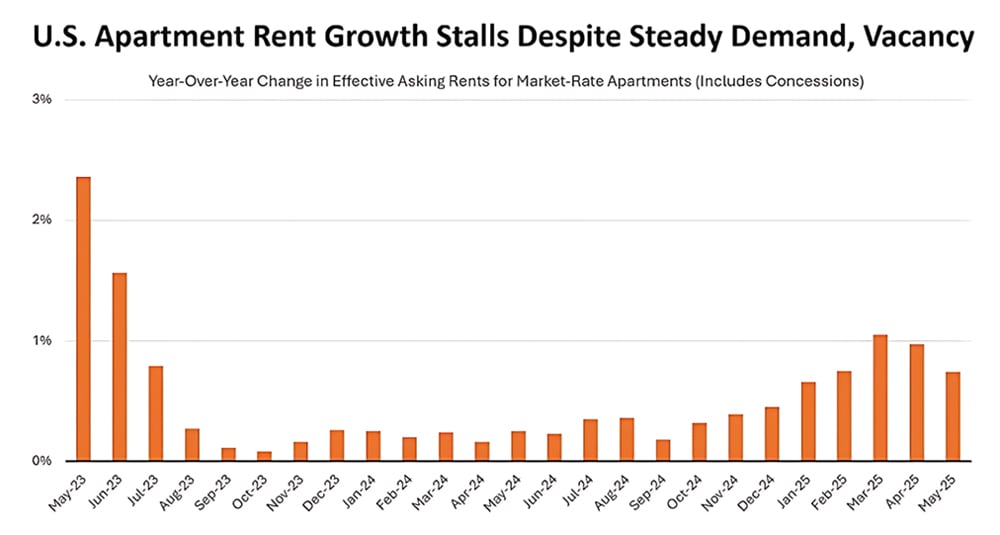

Following six straight months of increased rent momentum nationally, year-over-year rent growth has backtracked a bit in each of the past two months. Now in the heart of the leasing season, it seems the long-awaited rent rebound will have to wait a bit longer.

To be clear: It’s not a dramatic shift. Nationally, year-over-year effective rent growth eased from 1.05% in March to 0.74% in May. But it’s notable for a few reasons:

- It reversed upward rent momentum from the prior six

- It occurred during the heart of the leasing

- It came DESPITE strong absorption, steady occupancy rates, and improved affordability (declining rent-to-income ratios).

- And the kicker: It wasn’t limited to high-supply markets wrestling with heavy lease-up volumes. We saw stalled rent momentum EVEN IN LOW-SUPPLY

The latter point is key because it tells us something important: IT’S NOT JUST ABOUT SUPPLY RIGHT NOW. Supply at 40+ year highs is why rents flattened (or fell) across much of the country these past couple years, and supply is obviously still a factor in weak rent growth, but it doesn’t explain why rent growth backtracked in April and May following improved momentum previously.

Sources: Waymaker research, JPI research, FRED, RealPage Market Analytics

So, what happened? Is it because of weak leasing traffic?

Some operators I talk to point to soft leasing traffic.

But my response is: Were you expecting more? If so, you may have been too optimistic too soon. Even though supply is dropping off in terms of COMPLETIONS, we’re still smack in the middle of peak LEASE-UP volumes.

Apartment demand, at a macro level, remains well above normal. BUT you may not feel or see that at a portfolio level or at any individual asset. That’s just because all that demand is being spread across a greater number of properties (thanks to all the new supply).

Nationally, leasing traffic has been fairly stagnant for the last 18 months – at least in terms of year-over-year momentum, according to RealPage data. In some markets, it’s down year-over-year. (Radix, by comparison, is showing traffic down nationally.)

In other words: It’s still a VERY COMPETITIVE leasing environment – exacerbated by the fact that retention rates are sky high right now, taking many would-be apartment seekers off the market.

But vacancy rates (excluding active lease-ups) have held pretty steady. That’s partly, again, aided by high retention. So I’d weigh unspectacular traffic numbers with the reality that renewal demand is high, vacancy rates are stable and conversion rates appear to be up.

Indeed, Radix reported that tours are down year-over-year, but leases were basically flat. That supports anecdotal reports that we’re still seeing a good amount of motivated AND qualified leasing traffic (once you weed out fraudulent leasing apps). Not that we don’t see unqualified too, but point being that qualified leads are a) still there and b) converting.

And one more thing: Rent-to-income ratios are back down to pre-pandemic levels, and affordability has shifted to more a tailwind than a headwind, at least in the Class A and B markets. That’s not something you’d typically see amidst a market slowdown.

The Bottom Line: Apartment Operators are Nervous

We do not yet see any of the traditional tell-tale signs of a slowdown. Demand is strong, vacancy is stable, rent-to-income ratios are improving, and there’s no sign of any flight to affordability or of renters doubling up. The one variable more difficult to measure – operator sentiment. And my guess is that operators are nervous – understandably so – and prioritizing occupancy preservation over rents.

Washington, D.C., is a prime example of this trend. There’s been a lot of nervousness about the D.C. market due to DOGE cuts and federal layoffs. And yet apartment occupancy rates have held strong, improving 50 bps since January and now topping 96%. Rent-to-income ratios among new lease signers (in professionally managed, market-rate apartments) have fallen to 23.1%, according to RealPage data. The REITs with D.C. exposure have all reported solid demand and healthy collections there, too.

And yet: Rent growth in D.C. is backtracking more than most of the country. Year-over-year effective rent growth eased from 3.45% in March to 2.35% in May.

More Highlights on Apartment Trends:

- ApartmentList reported a similar trend as above, noting: “Despite rents ticking up for the fourth consecutive month, rent growth is currently slowing at the time of year when it typically ramps ”

- But all signs still point to strong demand for apartments. Yardi’s May report notes: “Uncertainty in the economy and financial markets has so far created minimal impact on multifamily fundamentals, which remained healthy in ” Yardi also noted “ongoing strong absorption,” though supply still exceeds demand in some markets.

- San Francisco has been one of the nation’s softest apartment markets since COVID hit in 2020, but it’s storming back in recent RealPage reported San Francisco ended lengthy streak of Midwest markets leading the nation in rent growth, with new lease effective rents jumping 6.2% year-over-year. The only other major markets above 4% were Chicago (5.5%) and New York (4.1%). Yardi, on the other hand, listed New York City as the leader for rent growth at 5.7%, followed by Kansas City at 4.0%.

- On the flip side, there’s more consistency at the bottom of the Austin once again posted the nation’s deepest rent cut among major markets at -8.0%. Consistent with the national story, that reflects backtracking after a stretch of moderating rent cuts. Two months ago, rents there were down 6.5%. Austin’s bottom was -8.3% in July 2024.

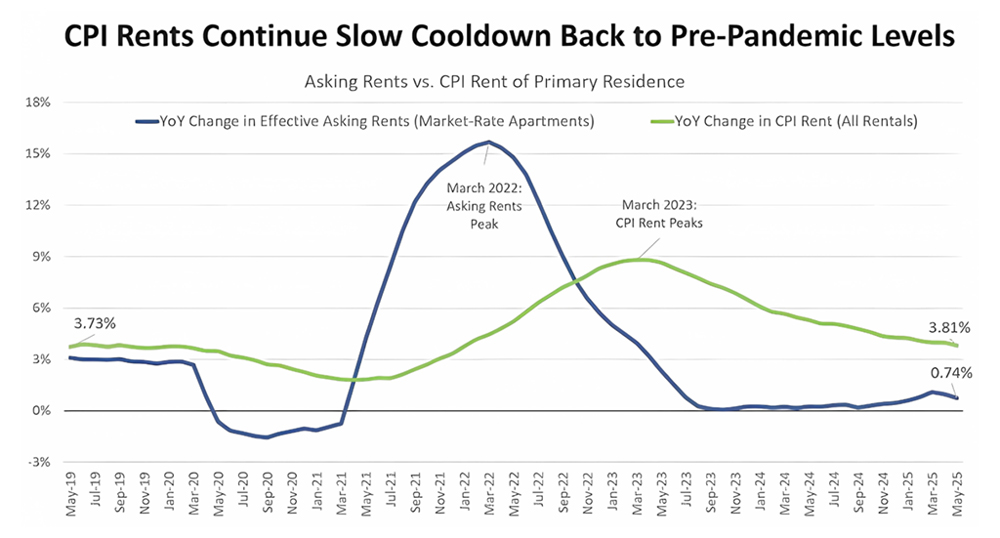

- CPI rent growth has cooled back down to pre-pandemic levels, coming in at 81% year-over-year in May. (See chart below.) That’s the lowest number in more than 3 years, and it’ll keep coming down. Remember: Rent plays an outsized role in CPI, but the way the U.S. Bureau of Labor Statistics measures rent includes low sample and heavy lags.

Sources: Waymaker research, JPI research, FRED, RealPage Market Analytics (effective asking rates covering market rate, professionally managed apartments)