June Multifamily Market Update: Trending in the Right Direction, But Not Very Fast

Through the spring and early summer, the U.S. apartment market continued to bounce back. But not a big bounce. It’s more like bouncing a partially deflated ball: The ball is going up, yes, but just not very high—not yet anyway.

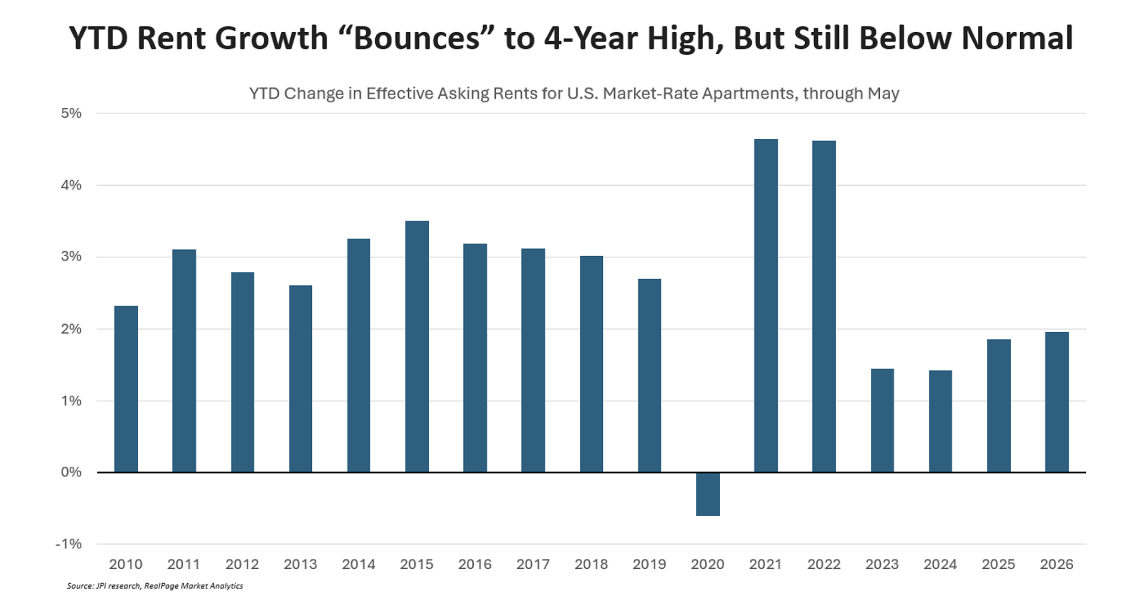

This chart showing year-to-date rent growth captures the partially deflated bounce-back perfectly: It shows YTD rent growth (through May) “bouncing” to a four-year high of nearly 2%, according to RealPage data. That’s progress, but it’s still well below normal. In the 2010s, apartments averaged nearly 3% rent growth over the same five-month period.

Why?

No, it’s not about weak demand. Apartment absorption isn’t at peak levels anymore, but it’s still above normal. (Of course, it would likely be even stronger if we had better job growth.)

No, it’s not about affordability. Rent-to-income levels (for market-rate apartment renters) is back to pre-COVID levels, as wage growth has topped rent growth for 40 consecutive months.

I know you’re probably tired of hearing this by now, but it’s still all about supply—at least for now. We are certainly nearing the tail end of the supply wave. Completions have dropped off dramatically (quarterly completions in Q1 came in 53% below the peak in Q3 2024).

But when we talk about supply pressures, that’s not just the number of units completing construction in any given period. It’s also the number of previously completed units still in active lease-up, meaning they’re physically completed but haven’t achieved stabilized occupancy. When properties are in lease-up, the owners are usually doing all they can to fill them, including rent concessions and even base rent cuts. Many renters who move into a newly built apartment are coming from another apartment. So, owners of existing apartments are trying to keep occupancy stable, too, which often means either cutting rents or increasing rents at a slower pace than usual.

Occupancy rates are slowly ticking upward across the market as new supply drops off and newly built apartments work through lease-up. Until lease-up numbers normalize and occupancy rates recover, it’ll likely remain a slog. When will that switch? I don’t know. But it’ll obviously vary by market and submarket, and I would expect the path to be bumpy—a “two-steps-forward, one-step-back” recovery pace.

Notably, CoStar’s Grant Montgomery recently wrote about this same trend: “The U.S. apartment market is beginning to stabilize as supply pressures ease, with improving conditions emerging in a growing number of markets.” He points out that some of the fastest-improving markets are high-supplied markets where rents are still falling but at moderating levels.

Market Highlights

Rent trends range dramatically based on market right now, with the common denominator being supply. Where supply is elevated, rents continue to decline, although the pace of declines is moderating. And where supply is very limited, rents are increasing. Here’s how I categorize some of the big markets:

Booming: San Francisco, San Jose, Virginia Beach

It’s old news to see San Francisco and San Jose on this list. But Virginia Beach has snuck up on the leaderboard, aided by very limited supply and very stable demand drivers. It’s not just a military town, as some wrongly perceive. Also worth noting: The Bay Area boom has spread to the East Bay. Oakland isn’t nearly as strong as San Francisco and San Jose, but it’s now topping 3% for rent growth.

Steady: Midwest, Northeast, Mid-Atlantic

The “steady Eddies” haven’t changed. New York City has moderated a bit from its red-hot days, but it’s still solid with 3% year-over-year rent growth.

Boston and Washington, D.C., remain an exception to the regional norm, with both posting slight rent cuts over the last year due to local demand-side challenges.

Green shoots: South Florida, Atlanta, Dallas, Orlando, Jacksonville, Salt Lake City

Rents are still falling due to high supply, but the pace is moderating in the low single-digits.

Looking for momentum: West Coast outside of the Bay Area

Rents remain pretty flat across the West Coast due to pockets of supply and, even more consequential, inconsistent demand. Orange County is one area that has seen some momentum of late.

It could be worse: Charlotte, Raleigh, Nashville, Las Vegas, Houston

Mixed stories across these markets, where rents are down 2% to 3.5% year over year. Houston’s challenges aren’t related to supply but soft demand—much softer than elsewhere in Texas. Charlotte, Raleigh, and Nashville all have heavy supply, but rents haven’t fallen as sharply as places like Austin or Phoenix.

It’s still rough out there: Austin, Denver, Phoenix, Tampa, San Antonio

It’s the usual suspects plus Tampa, which has lesser supply pressures than the other four but conspicuously soft demand of late.

Other Highlights

Yardi Matrix reports: “While the seasonal pattern remains intact, the spring leasing season is generating less pricing power than it did historically.” Yardi writes that “while elevated supply remains the primary driver,” softer leasing and higher inflation are contributing factors.

CoStar is acquiring Zonda, “a leading provider of new home construction data, homebuilder software, and residential real estate marketplaces, for $800 million in cash.” Zonda covers multifamily as well as single-family homes.

U.S. Census data shows a big drop in multifamily starts, but this is no surprise to anyone paying attention. Remember, the Census Bureau just samples a small share of permit holders to ask what started and extrapolates from there. Private sector data providers tend to do a much better job tracking starts.

Apartment List published an interesting research article noting that while young adults are less likely to become homeowners today, a big chunk of them are “not really a renter,” either.