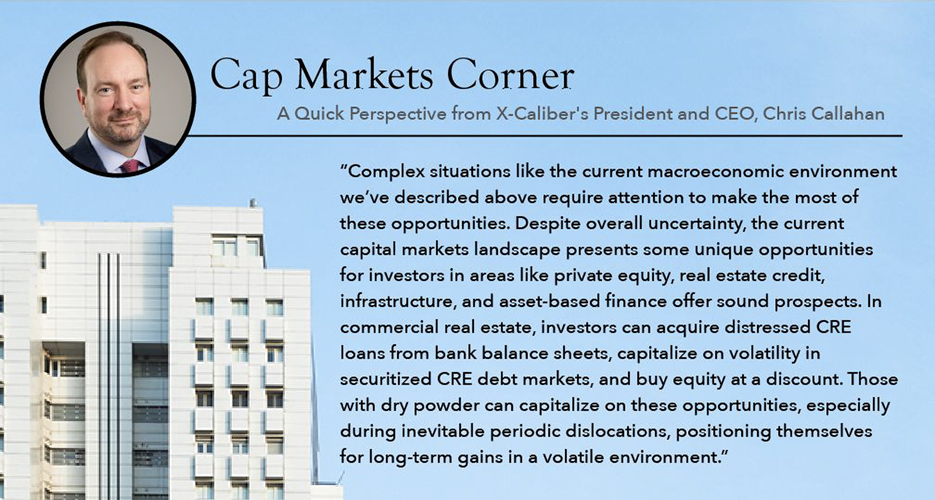

X-Caliber July 2024 Market Movers

Capital Market Matters: The Fed Speaks Again

Off in Portugal, at a panel discussion for the European Central Bank, the most powerful central banker in the world put together two thoughts, according to CNBC, that are bound to disappoint. Part one, “The last [inflation] reading and the one before it to a lesser, lesser extent, suggest that we are getting back on the disinflationary path,” CNBC reported Jerome Powell as saying.

The second: “We want to be more confident that inflation is moving sustainably down toward 2% before we start the process of reducing or loosening policy.”

Once again, the Fed is where it was just a few months ago. 1. Things are improving. 2. We’re on a disinflationary path. 3. Sorry, but we have to be sure. You’re not in a hurry, right?

Earlier this year, when people wanted to know why there wouldn’t be cuts in March, some long-time Fed watchers and former insiders showed their frustration at the bank insisting on gathering nine to 12 months of data so they could feel comfortable about whatever decisions they made.

The same thing is happening again, and you can’t reasonably blame them. In the 1980s, inflation was high and volatile. Interest rates went up, inflation started to cool, the Fed started to bring rates down, and the doubling back of inflation was massive.

They don’t ever want to make the same mistake again, and contrary to many popular opinions, the Fed has been pushing back on politicians who tried influencing monetary policy for most of the central bank’s nearly 115-year existence.

Right now, be patient. Plan on everything taking longer. Work intelligently and carefully. Invest now to get a foot into promising deals that might not be possible in a year or two.

CRE Insights: Sales Trends

Sometimes looking at a property segment that isn’t what you normally consider can bring a new perspective. A slight diversion from what is normally the big message can let you appreciate things anew and, in this case, anticipate where markets might be moving.

Goldman Sachs analyst Caitlin Burrows released a recent analysis saying that the worst may be over for commercial real estate transactions, as Benzinga reported. She said that some signs suggest that, at least for office, the market may finally have bottomed. Why discuss office if you don’t focus on it? Because it has become the riches-to-rags story in the overall industry. Even as, say, multifamily has taken its licks, people still need to live someplace. As it turns out, workers don’t necessarily need to be in the office that often. If office might be hitting bottom, what hasn’t?

Burrows pointed to the Global Financial Crisis. It took purging problems through eight, year-over-year quarterly transaction declines before there was some improvement in the ninth quarter. She said that the Organisation for Economic Co-operation and Development has its U.S. Composite Business Confidence Index, which typically leads office leasing volumes by about two quarters, has been improving.

Inventory has been increasing in multifamily, with 2023 being one record year and 2024 looking as though it would top even that. But that depends on location, as much of the oversupply has been focused on high-growth areas like the South and Southeast. Other areas can be tight. Yardi Matrix says that activity may remain weak — again on average, not by particular geographic segment — but could rebound in the second half of the year. It’s a good time to start scouting deals and where business is likely to grow.

On the Horizon: Cred iQ Distress Rate Hits Third Consecutive Record

If one distress record is bad and a second consecutive one is worse, what do you call a third distress record? Time to make a deal.

CRED iQ last month announced that its distress rate for all property types had hit a third consecutive record. The firm’s special servicing stood at 8.09% while the delinquency rate was at 5.8%. In April, the multifamily distress rate hit 7.1% in May, down a touch from April’s 7.2% but both months way up from the 3.7% March figure. Much of that was due to a big loan — $1.75 billion backed by Parkmerced with 3,221 units in San Francisco. It was a non-monetary default.

Understanding the information takes some nuance. “Looking at payment status, 24.4% of the loans are current, with an additional 2% and 5.5% attributable to Late (but in the grace period) and Late (but less than 30 days) respectively,” the firm wrote. “Once again, the largest category was Non-Performing Matured at 35%, followed by 90+ Days Delinquent at 15.6% and Performing Matured at 11.8%.”

There are deals to be had and things aren’t as dire as they might seem.